When something collapses, new opportunities open up. Hedge funds, private equity firms, and other asset managers specialize in this. And now there are signs of hope for these folks, that opportunities are approaching, that the credit bubble is about to implode, offering untold riches to those able to pick up the right scraps.

How do we know? Wall Street firms are staffing up for the coming era of “distressed debt.”

This is an ad I ran into on S&P Capital IQ LCD’s highyieldbond.com:

And the first of the “Key Accountabilities” is this:Taplin, Canida & Habacht is looking for a High Yield/Distressed Debt Corporate Analyst. The analyst will be a generalist, looking for opportunities across sectors and issuer capital structures.

The firm, which manages fixed income portfolios for institutional investors, may look to profit from other funds’ misery by buying up distressed debt for cents on the dollar, hoping to score some big gains when the dust settles.Monitor and analyze credit risk and recovery value of high yield and distressed debt sectors through sector analysis, bottom-up fundamental research and bond covenant analysis.

It’s not the only firm looking for the right people. According to efinancialcareers, the Number 2 of the 10 most sought-after specialists in New York’s financial services sector for “the remainder of 2015” is – after “Healthcare-focused investment bankers” – well… “Distressed debt analysts.”

So the report:

“Distressed debt” is one of the few growth industries in the US. More and more junk bonds are falling into this category, and their prices are deteriorating.Maybe this isn’t a great indication of the state of the economy, but hedge funds with a distressed debt focus are looking to staff up. Primarily, they’re looking for experienced analysts with 8-15 years in the industry, suggests Robin Judson, managing partner and group founder at headhunters Robin Judson Partners in New York.

“This is in anticipation of more credits running into problems over the next 18 months,” she says.

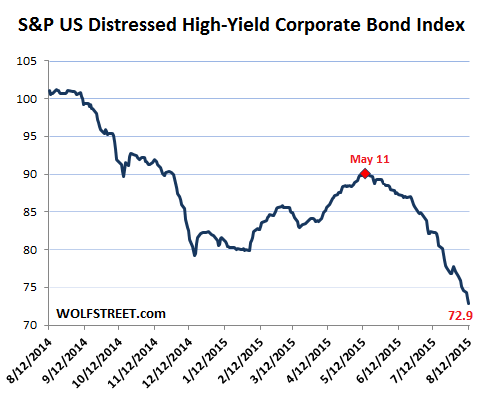

These distressed bonds are tracked in special indices, including the S&P US Distressed High-Yield Corporate Bond Index. It’s a market-weighted index of junk bonds with an option-adjusted spread of at least 1,000 basis points (10 percentage points). This massive spread indicates that investors believe that these bonds are in a heap of trouble.

August has been rough for distressed bonds. Month-to-date, the index has dropped 5.4% to 72.89. Since mid-May, the peak of the false-hope energy-bond rally, the index has lost 19%. A year ago, the index was at 101. It has since lost 28%. The chart shows the brutality of the decline:

Note the energy-driven panic last fall, followed by the false-hope energy-bond rally in the spring until May 11. But it wasn’t just energy bonds. Many troubled companies – opportunities or nightmares, depending where you sit – ply their trade outside energy. Example du jour: American Apparel.

The company’s shares have been in the penny-stock range since 2010. It has a stellar record of losing money. Tuesday afterhours, it warned in an SEC filing that it didn’t have enough cash to get through the next 12 months, and that it might not find any investors stupid enough to lend it more money to burn through. Well, OK, it didn’t phrase it exactly that way.

Its shares crashed 50% in early trading on Wednesday, but then recovered some to end the day down 37%, having fallen from almost nothing ($0.20 a share) to even less ($0.13 a share).

To stay afloat over the years, it piled on new debt to make up for the money it was losing. Then there was corporate turmoil, including the termination for cause of its CEO and founder Dov Charney.

For shareholders, this company has been hopeless for years. But some of its debt still has value. Standard & Poor’s graciously rates the company CCC- with negative outlook. And it rates the 13% senior secured notes due 2020 at CC, with a recovery rating of 5. Moody’s rates the company Caa2, also with negative outlook.

If the company, which had $271 million in assets and $415 million in liabilities as of March 31, runs out of cash, defaults on its debt, and restructures in bankruptcy court, its shares will be worthless, and its unsecured creditors will get shafted too. But its secured debt still has some value. The fund managers that own it might want to get rid of it before it’s too late. And that’s where hedge funds and private equity firms with some “distressed debt analysts” under their roof might see an opportunity, for cents on the dollar...MORERelated:

As Blackstone Pushes Liquid Alts At the 'Little Guy', Hedgies Wait To Short Them